Ron Paul Takes Lead In Iowa

When we learned on Saturday that

the Des Moines Register, owned by Gannett - whose Chairman just

happens to be a Private Equity firm head, and worked at Citigroup for

most of her career, has endorsed Mitt Romney for president we said that

this development "while likely set to provide a very short-term boost

to Romney's chances, it is the baseless ongoing accusations against

Ron Paul that will likely solidify the groundswell behind the Texan,

with such desperate platitudes as "Ron Paul's libertarian ideology

would lead to economic chaos and isolationism, neither of which this

nation can afford." As it turns out, according to the latest Public

Policy Polling data we can skip the kneejerk reaction and go straight

to the after effect, because as of the latest polling, Ron Paul has finally taken the lead in Iowa. Granted

this is just one of many polling organizations, and potentially it may

be biased, but the bottom line is that often time reality (objective

and subjective) is self-reinforcing. And when the US public realizes

that the only candidate who deserves to be in the White House has a

running chance, they will flock to him. Suddenly backing Ron Paul may

just become the next cool thing. As for the Gingrich "honeymoon", it

was over well before the nth divorce (pardon the pun). At

this point we can only hope that the electoral game of reverse American

Idol where the poll head is voted off in a week or so stops with Paul.

However, with Perry, Bachmann, Romney and Gingrich already having been

voted off, the only possible dark horse now remains Huntsman - does he

have a running chance against Paul?

When we learned on Saturday that

the Des Moines Register, owned by Gannett - whose Chairman just

happens to be a Private Equity firm head, and worked at Citigroup for

most of her career, has endorsed Mitt Romney for president we said that

this development "while likely set to provide a very short-term boost

to Romney's chances, it is the baseless ongoing accusations against

Ron Paul that will likely solidify the groundswell behind the Texan,

with such desperate platitudes as "Ron Paul's libertarian ideology

would lead to economic chaos and isolationism, neither of which this

nation can afford." As it turns out, according to the latest Public

Policy Polling data we can skip the kneejerk reaction and go straight

to the after effect, because as of the latest polling, Ron Paul has finally taken the lead in Iowa. Granted

this is just one of many polling organizations, and potentially it may

be biased, but the bottom line is that often time reality (objective

and subjective) is self-reinforcing. And when the US public realizes

that the only candidate who deserves to be in the White House has a

running chance, they will flock to him. Suddenly backing Ron Paul may

just become the next cool thing. As for the Gingrich "honeymoon", it

was over well before the nth divorce (pardon the pun). At

this point we can only hope that the electoral game of reverse American

Idol where the poll head is voted off in a week or so stops with Paul.

However, with Perry, Bachmann, Romney and Gingrich already having been

voted off, the only possible dark horse now remains Huntsman - does he

have a running chance against Paul?Watch Mario Draghi Predict The Future

... Because when it comes to forecasting, central planners rock.

... Because when it comes to forecasting, central planners rock.

Will Congress Kill The Payroll Tax Extension - Advance Look At Today's 6:30PM Vote

Tonight at 6:30 pm the House is set to vote on the Senate’s payroll tax cut/unemployment insurance bill. As it stands right now, it appears likely that the vote will fail due to lack of support by Boehner and other house leaders. Furthermore, Senate has said it will not present an alterantive bill (as of yet). Which means that with a major portion of Q1 GDP at stake (non-renewal of payroll cuts means up to 1% of GDP being cut in Q1 2012), the futures market will be very focued on newsflow after the close. Here is Goldman's rundown of what to expect tonight in DC.As Liquidity Swap Impact Fades, ECB Is Back To Propping Up Peripheral Bond Markets In Size

Last week, in the aftermath of the global coordinated liquidity swap facility expansion (OIS+100 to OIS+50) from November 30, with the added benefit of the contemporaneous Chinese RRR cut, bond yields plunged on short-term hope that the Fed's action would be a long-term solution for the Eurozone. It wasn't. But not before the ECB received a brief respite from manipulating bond markets. As a result of the November 30 action, the ECB proceeded to buy just €635 million of Peripheral (read Italian) bonds as the BTP yield plunged. Days later, following the realization that this is nothing but yet another band aid mechanism, yields once again soared, and depending on the benchmark used, pushed beyond 7% once again. In the meantime, the story of the ECB's 3 year LTRO rescue, lost in the aftermath of the Fed action, was resurrected, and is now attributed by some as being some pseudo bazooka that will rescue the ECB. It won't as was explained yesterday. And sure enough, one week after the knee jerk reaction from the liquidity intervention, the ECB was once again out in full force picking up pennies in front of the steamroller, buying up €3.361 billion in bonds in the week ended December 16, which brings the total purchases at €211 billion (net of maturities).

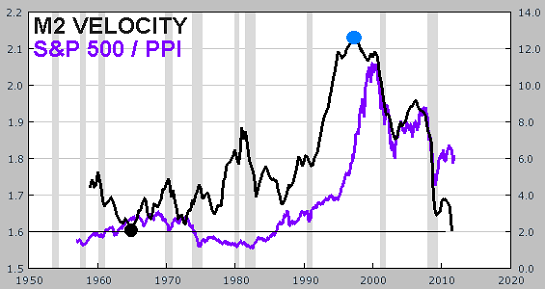

Guest Post: Three Charts That Blow The Doors Off Any Hope Of A 2012 Rally

A good way to generate hate mail is to question 1) Santa's "guaranteed year-end rally" and 2) the notion that market rallies always resume soon enough because of the Federal Reserve's backstop/intervention. If we step back from the latest shuck-and-jive data from the Ministry of Propaganda, a.k.a. the Status Quo managing perceptions, and take a longer view of the economy, money, credit and the stock market, we get an extremely troubling set of insights. Courtesy of this site's Chartist Friend from Pittsburgh, here are three charts that completely undermine the fantasy that central planning/intervention can "save the market" once again in 2012 and beyond.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

No comments:

Post a Comment